Casey Mulligan has a response on his blog to a recent Bloomberg View column of mine about wages and the "Great Vacation" hypothesis. In that column, I basically just said that flat real wages are a puzzle for explanations of the post-2009 stagnation that rely on government paying people not to work (the "Great Vacation" idea). Casey doesn't like this. Let's go through his points...

Naturally, a supply-demand decomposition exercise is enhanced by looking at both the quantity and price of labor, also known as the wage rate. That's why my book on the recession starts off with various indicators of wage rates and their dynamics (see chapter 2 beginning on page 9).Well then I guess my article was not exactly news to Casey.

Three or four decades of labor economics research are of great assistance in this exercise.Well, I guess they've got to be good for something.

I kid, I kid!

[A] reduction in labor supply could be associated with reduced cash earnings even while it was increasing employer costs:

1. A reduction in labor supply could reduce the quality of labor, with workers putting in less effort, or doing less to maintain their skills, or become less attached to the labor market. This tends to reduce cash earnings per hour because each hour is less productive. These have been major factors in the analysis of women's wages, where most economist believe that women's hourly earnings increased as a consequence of supplying more (see Becker 1985, Goldin and Katz 2002, Mulligan and Rubinstein 2008, and many others). See also some of the literature on unemployment insurance such as Ljungqvist and Sargent's paper on European unemployment.True, but don't things like unemployment benefits and Social Security Disability only go to the unemployed? Slacking off at your job does not result in the government mailing you a check. Why would a rise in welfare-type benefits cause people to slack more? Are they sitting there at their desks feeling depressed, thinking "Dang, I could be earning almost this much if I quit my job"? I guess it's possible, but unlikely, especially given the decreased rate of quits in recessions.

A reduction in labor supply or demand could increase the average quality of labor through a composition bias. See p. 17ff of my book and the references cited therein.Wouldn't this tend to increase wages, or am I being dense? Do I have to go to p. 17ff?

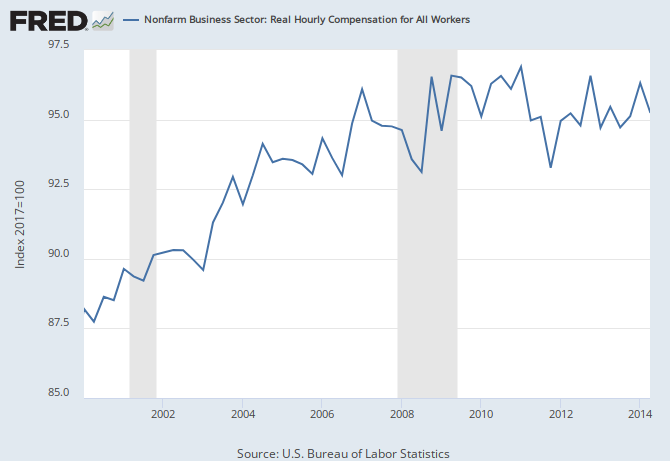

Because of fringe benefits, cash hourly earnings are not the same as employer cost. As employer health insurance expenditure has been growing over time, the growth of cash hourly earnings has substantially under-estimated the growth of employer cost.OK, but did these non-cash benefits start to increase more in the years following 2009? Nope. They flattened out just like wages. So the point I made in my article applies to this kind of compensation as well.

Labor economists have also long studied the incidence of supply and demand impulses: that is, the effects of supply and demand factors on both wage rates and the quantity of labor. The consensus is that: (a) labor demand is more wage elastic than labor supply and (b) labor demand is even more wage elastic in the long run than it is in the short run.

Suppose that the reduction in the quantity of labor were 50% due to demand factors and 50% due to supply factors, and that we had overcome all of the measurement issues cited above. Result (a) means that wages would fall in the short run, because supply shifts translate more into labor quantity than into wage rates while, in comparison, demand shifts translate more into wage rates than labor quantity. In this example, it would be wrong to conclude from reduced wage rates than supply is less important than demand for explaining the change in the quantity of labor.

To put it another way, if we found that wage rates (properly measured) were constant, but didn't know the relative contribution of demand and supply factors to the quantity change, result (a) tells us that the majority of the labor quantity change was due to supply factors. With a labor supply elasticity of 0.5 and labor demand elasticity of -3 (reasonably conservative short run estimates), the constant wage rate result means that 86 percent of the quantity change was due to supply factors and only 14 percent due to demand factors. In the long run, labor demand is even more wage elastic, and the share attributable to labor supply is even closer to 100%.

To put it yet another way, if it were true that labor demand explained the majority of the change in labor quantity, then employer costs (properly measured) would have fallen dramatically.I think it's very important to correct for the trend here. Real wages have been flat since the crisis and recession, it's true, but were growing strongly before that. Also, continued productivity growth since the recession seems to indicate that real wages have fallen substantially relative to the long-term trend.

{kind=link}

As for the inelasticity of labor supply, it had always been my understanding that the macro evidence showed a fairly high elasticity of labor supply. You'd certainly expect Mulligan, whose theory of unemployment is based on a rise in implicit taxes arising from benefit phase-outs, to take this view. Without looking at his parametrization, I can't tell if the "inelastic labor supply" story is numerically consistent with the "benefit phase-outs caused the stagnation" story, but the two stories do seem to be somewhat at odds. In other words, if you think unemployment is due mainly to people being paid not to work, then it seems like you have to think that people's work decisions respond a lot to how much you pay them.

As for the long run, the period we're talking about is something like 2009-2012, so it doesn't seem that long to me.

In other words, the flattening of wages since the recession still seems like a puzzle for these theories. And I didn't even mention sticky real or nominal wages...

(Note: I was a little unfair in lumping Mitman's theory in with the "supply shock" stories, because his model uses search frictions to make unemployment insurance reduce labor demand. I still think his model is probably pretty wrong, though!)

No comments:

Post a Comment